Japan just quietly dropped a blueprint to overhaul its 50-year-old payment infrastructure by 2030

Japan just announced it's replacing the backbone of its entire banking system.

The Zengin System has been running since 1973. That's over 50 years.

It connects 1,071 financial institutions. It processes nearly every domestic bank transfer in the country.

And now, a government-backed study group says: it's time to build something new from scratch.

Here's why this matters — and what's coming next.

The problem isn't that Zengin is broken. It's that the world moved on.

Countries like the US (FedNow), EU (TIPS), UK (FPS), AU(AUNPP), Singapore (FAST), India (UPI), and Thailand (PromptPay) have all launched modern real-time payment systems.

These systems offer features that Zengin simply can't support: pre-transfer account verification, instant deposit confirmation, mobile number-based transfers, QR code payments, and payment requests.

Japan's system? Still running on one-way communication. Fixed-length message formats. No native support for ISO 20022 — the global standard every major economy is adopting.

The study group's own words: the gap with overseas systems is widening, not shrinking.

The structural issues go deep.

Zengin uses legacy architecture that's been patched and extended for decades. This has created three compounding problems:

First, complexity. Years of add-on features and regulatory patches have made the system design so intricate that finding and fixing issues — like the October 2023 relay computer outage — takes far too long.

Second, cost. Maintaining this complexity is expensive. Failed transfers due to non-mandatory account verification waste human resources. A web of sub-clearing systems (ZEDI, J-Debit, CAFIS, Cotora, Multi-Payment Network) each require separate maintenance budgets.

Third, inflexibility. The system can't attach rich data to transactions. It can't connect to stablecoin or tokenized deposit networks. It can't easily comply with the revised FATF Recommendation 16 on cross-border payment transparency, which has a 2030 deadline.

Upgrading the current system isn't viable. The study group concluded that building new is actually cheaper and more adaptable than continuing to patch what exists.

So what's the plan?

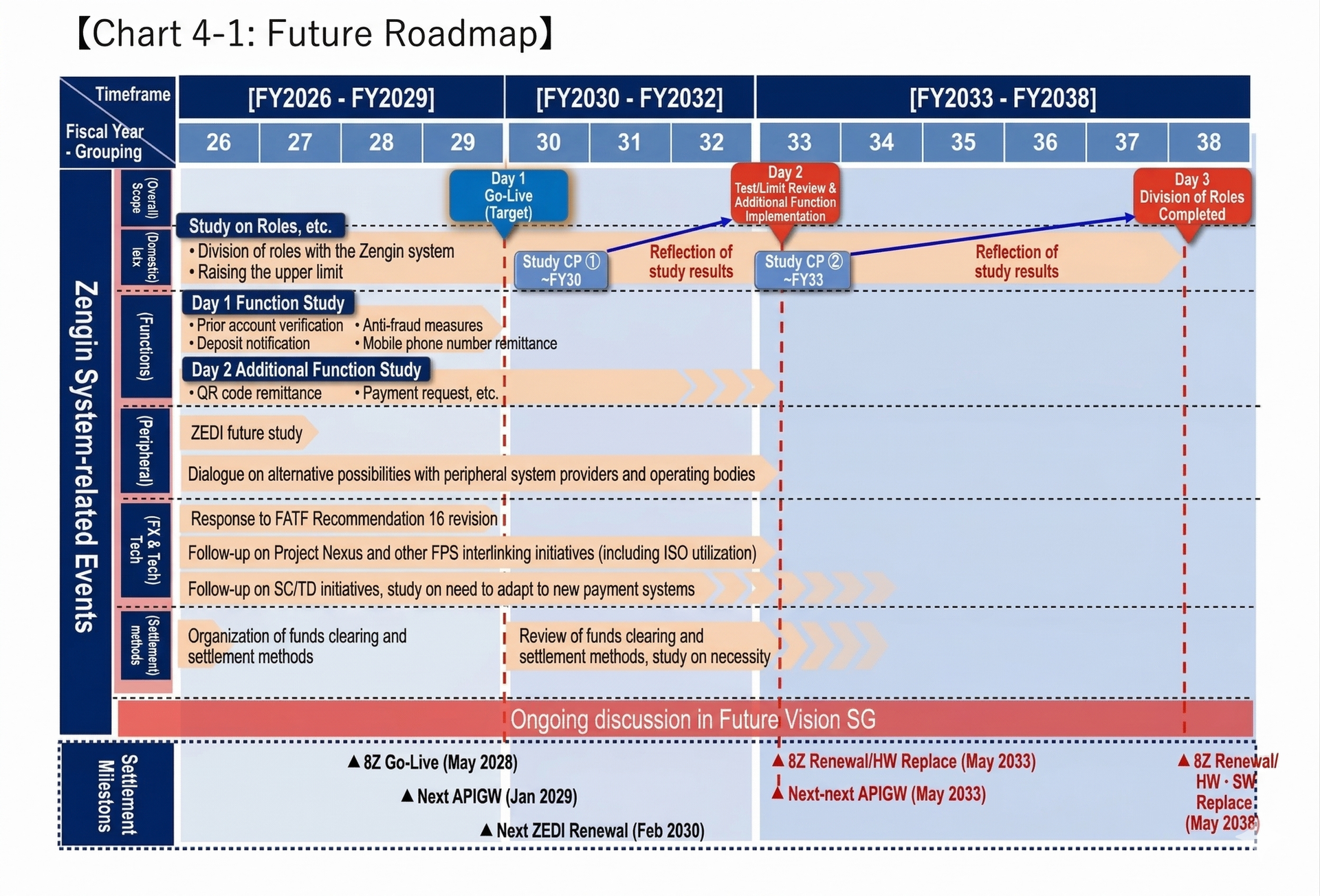

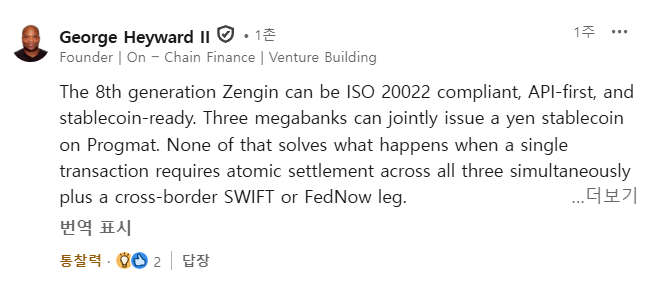

The new system targets a 2030 launch. Here's what it's designed to deliver:

Real-time, 24/7 settlement — true instant payments with deposit confirmation, not just "24/7 availability."

Mandatory pre-transfer account verification — every single transaction, no exceptions. This is positioned as a core fraud prevention measure.

ISO 20022 messaging — the global standard, enabling richer data and cross-border interoperability. But with conversion tools so banks don't have to overhaul their core systems on day one.

API-first, bidirectional communication — replacing the current one-way model. This unlocks real-time status queries, error handling, and future service integrations.

Alias-based transfers — send money using a phone number or email, powered by a new Proxy directory.

Cross-border readiness — designed to connect with Project Nexus (the BIS-backed initiative linking fast payment systems across Singapore, Thailand, India, Malaysia, Philippines, and Indonesia). The system won't require this connection at launch, but it will be architecturally ready.

Stablecoin and tokenized deposit extensibility — not built into the core, but the architecture will support external system integration as these technologies mature.

The transition strategy is pragmatic, not reckless.

The new system will run alongside Zengin initially. Banks can start as "receive-only" participants to lower the entry barrier. Transfer limits will start below ¥100 million per transaction and scale up over time — similar to how FedNow started at $500K and expanded to $10M.

Bulk payments like pensions and stock dividends stay on the old system for now. QR code payments and payment requests are deferred to a Phase 2 around 2033.

By 2038, when Zengin's next hardware refresh is due, the goal is to either significantly downsize or fully consolidate into the new platform.

A critical checkpoint is set for 2033 to evaluate progress and adjust course.

The bigger picture.

This isn't just a technology upgrade. It's Japan positioning its financial infrastructure for the next era — where AI agents execute payments, where digital assets need settlement rails, and where cross-border transfers between Asian economies happen in seconds, not days.

The RFI goes out in the first half of FY2026. RFP in the second half. Build-or-no-build decision by end of FY2026.

If you work in payments, fintech, banking infrastructure, or cross-border finance — this is one of the most significant national payment system rebuilds happening anywhere right now.

Worth watching closely.

After sharing above on linkedin there were some intersting perspectives added in the comment section.

Executive summary in EN

https://www.zengin-net.jp/en/announcement/pdf/announcement_20260319.pdf

For original 41 page study group announcement -Japanese

https://www.zengin-net.jp/announcement/pdf/announcement_20260319-2.pdf

3 page summary -Japanese

https://www.zengin-net.jp/announcement/pdf/announcement_20260319-3.pdf

Member discussion